Not all car insurance policies provide the same level of protection, and broad form car insurance is one of the most misunderstood coverage options available in the U.S. While it can be a budget-friendly choice for some drivers, it often offers limited protection and may not cover every vehicle or situation you expect. Auto Insure News takes a closer look at how this type of policy works, its biggest advantages and drawbacks, and the situations where it may not make sense.

What is broad form car insurance?

This section defines broad form car insurance and distinguishes it from a conventional automobile policy. As a form of named driver car insurance, it is constructed around the individual operator rather than around the household or the insured vehicle.

Broad form car insurance may be defined as a limited, lower-cost automobile policy that provides liability protection to one named driver. When the named driver is at fault in a collision, the policy may pay for the resulting injuries or property damage sustained by third parties, subject to the applicable coverage limits. The defining characteristic of the policy is its single-driver structure: protection attaches to the listed person rather than to the vehicle, and consequently, other operators are generally excluded.

It is important to distinguish this product from two related concepts. First, broad form car insurance is not equivalent to a “full coverage” policy, which additionally protects the insured vehicle. Second, it is not the same as a standard family automobile policy, which can be structured to cover multiple household members. The principal advantages of broad form coverage are its lower cost and administrative simplicity; the corresponding disadvantage is its narrower scope of protection.

The three forms of automobile insurance: standard, broad, and limited

To place broad form coverage in context, it is useful to recognise how different types of car insurance are commonly classified, including standard, broad, and limited forms. Each form represents a distinct balance between premium cost and breadth of protection, and limited form insurance in particular is frequently mistaken for broad form coverage despite differing substantially in what it pays.

- Standard form: The conventional policy most drivers purchase. It may combine several coverages: liability, collision, comprehensive, uninsured/underinsured motorist protection, and optional add-ons, and can list multiple vehicles and drivers.

- Broad form: A liability-oriented policy that follows a single named driver. It is less expensive than a standard policy because it provides significantly narrower protection and excludes collision, comprehensive, and coverage for other drivers.

- Limited form: A restricted policy that pays only when the insured is not at fault in an accident. Although inexpensive, limited form coverage typically does not satisfy state minimum requirements and is therefore suitable only in narrow circumstances.

| Form | Protection | Meets state minimum? | Relative cost |

|---|---|---|---|

| Standard | Broadest; multiple coverages, drivers, and vehicles | Yes | Highest |

| Broad | Liability for one named driver | Generally, yes, where offered | Low |

| Limited | Pays only when the insured is not at fault | Usually no | Lowest |

How broad form car insurance works

In practice, broad form coverage functions as auto liability coverage that follows the named insured rather than automatically protecting every driver of the insured vehicle.

Under a standard automobile policy, the insurer covers the vehicles and drivers listed on the declarations page. A broad form policy modifies this model by insuring the named driver across the vehicles that person owns or is authorised to operate. If the named driver causes an accident, the liability component may pay for the other party’s medical expenses and property repairs, up to the policy limits. Industry sources note that automobile liability coverage generally pays for damage the insured causes to others, encompassing both bodily injury and property damage.

What broad form car insurance covers

In most cases, the policy provides a level of minimum liability insurance, although the precise scope depends on the insurer, the governing state, and the policy language.

The coverage afforded by broad form liability protection is concentrated in two areas: bodily injury liability and property damage liability.

Bodily injury liability

Bodily injury liability may pay for injuries the insured causes to another person in an at-fault accident. Covered costs can include medical treatment, emergency care, lost wages, and, in some circumstances, legal expenses arising from a claim. The amount payable is governed by the policy’s stated limits.

Property damage liability

Property damage liability may pay for damage the insured causes to another party’s property, most commonly another vehicle, but potentially including fences, signage, buildings, or other structures. The Washington State Office of the Insurance Commissioner explains that property damage liability assists in paying for damage the insured causes to another vehicle or to property in an accident.

Summary of typical coverage

| Coverage type | Usually included? | Explanation |

|---|---|---|

| Bodily injury liability | Usually yes | Pays for injuries the insured causes to others |

| Property damage liability | Usually yes | Pays for damage the insured causes to others’ property |

| Named driver coverage | Yes | Protects the single person listed on the policy |

| Other drivers | Usually no | Other operators are generally not covered |

| Collision coverage | Usually no | Damage to the insured’s own vehicle is not covered |

| Comprehensive coverage | Usually no | Theft, vandalism, weather, and animal damage are not covered |

| Uninsured motorist coverage | Varies | May be optional, required, or unavailable by state |

| Medical payments / PIP | Varies | Depends on state law and insurer options |

What broad form car insurance does not cover

This section examines the policy’s exclusions, which are as significant as its inclusions. The lower premium associated with broad form coverage is largely attributable to the omission of protections such as collision coverage and comprehensive coverage.

A broad form policy generally does not pay for damage to the insured’s own vehicle, nor does it extend protection to other operators. A clear understanding of these exclusions is essential because the assumption of coverage that does not exist can result in substantial uninsured losses.

Exclusion of other drivers

The most consequential limitation is the exclusion of other drivers. If a spouse, child, roommate, or colleague operates the insured vehicle, that individual may not be covered, even with the policyholder’s permission, because protection is restricted to the named driver. For households with multiple operators, a standard automobile policy that lists additional drivers is generally more appropriate.

Exclusion of damage to the insured’s own vehicle

Because liability insurance is designed to compensate third parties for harm the insured causes, it does not automatically repair or replace the insured’s own vehicle. Protection of one’s own automobile generally requires collision coverage, which addresses crash-related damage, and comprehensive coverage, which addresses non-collision events such as theft, fire, hail, vandalism, and animal strikes.

Financed or leased vehicles

When a vehicle is financed or leased, the lender or lessor will ordinarily require physical damage coverage, typically collision and comprehensive. Drivers should understand how a lease on a car works before choosing a liability-only broad form policy that may violate lease requirements. A liability-only broad form policy may not satisfy these contractual requirements, and selecting it could place the policyholder in violation of the loan or lease agreement.

Additional exclusions: vehicle types, passengers, and endorsements

Beyond collision and comprehensive coverage, a broad form policy typically excludes several further categories of protection. Because the policy is confined to third-party liability for a single operator, it generally provides no coverage for the policyholder’s own passengers and cannot be supplemented with common endorsements.

- Specialised vehicles: Motorcycles, recreational vehicles (RVs), all-terrain vehicles (ATVs), and commercial vehicles are generally not covered. Drivers using a vehicle for business should review who needs commercial auto insurance instead of relying on a broad form personal policy.

- The policyholder’s passengers: Injuries to the insured’s own passengers are typically not covered, absent medical payments or personal injury protection.

- Theft and vandalism: Loss of personal property from the vehicle is not covered; a renters’ or homeowners policy may apply instead.

- Endorsements: Rental reimbursement, roadside assistance, and gap insurance are typically unavailable.

- Higher liability limits: The option to purchase additional liability coverage above the state minimum is generally not offered.

Limited availability

Broad form car insurance is not offered in every state, and even within permitting states, not every insurer provides it. State statutes, insurance regulations, and individual underwriting practices all influence availability.

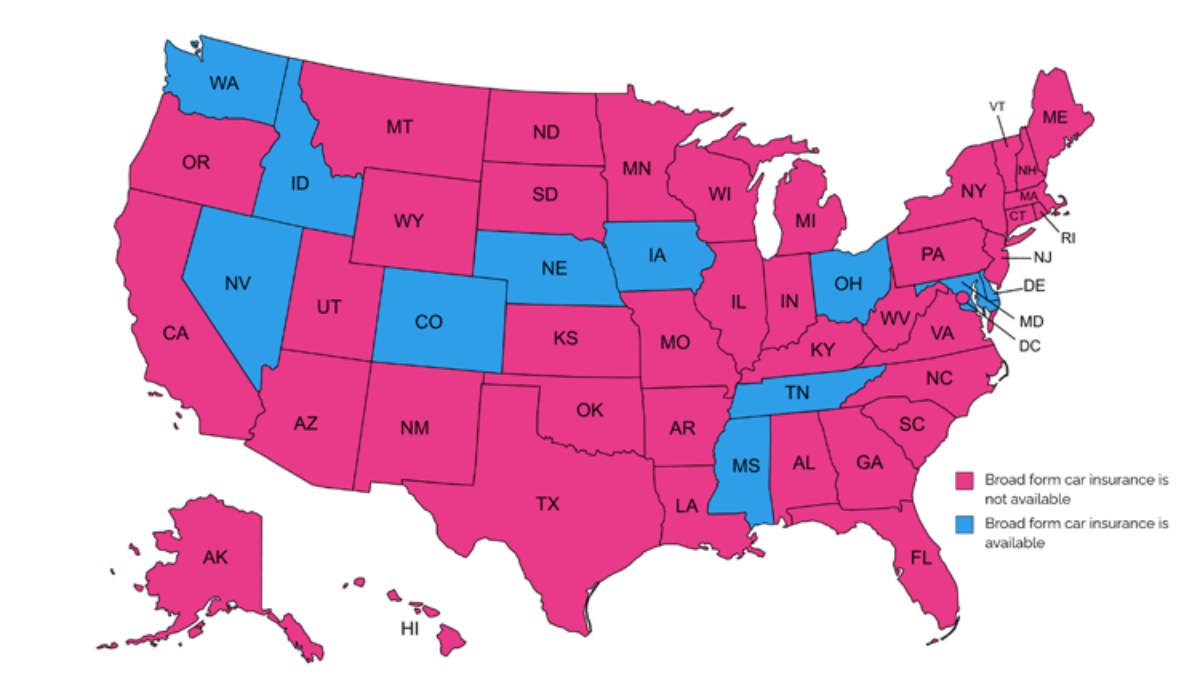

Where is broad form car insurance available?

This section identifies where the product may be purchased. The list of broad form car insurance states is limited, because the narrow, single-driver structure is permitted only in certain jurisdictions.

As of 2026, broad form car insurance is available in the following eleven states:

- Colorado

- Delaware

- Idaho

- Iowa

- Maryland

- Mississippi

- Nebraska

- Nevada

- Ohio

- Tennessee

- Washington

Even within these states, major national insurers seldom market the product. Broad form coverage is most often offered by nonstandard or high-risk insurers, such as Dairyland and Bristol West, that specialise in minimum-level, lower-cost policies. Drivers residing outside these eleven states cannot purchase broad form coverage and should instead evaluate standard liability or non-owner alternatives.

How much does broad form car insurance cost?

Broad form coverage is frequently marketed as affordable auto insurance because it insures fewer risks than a conventional policy, but a lower premium reflects reduced protection rather than superior value.

There is no single price for broad form coverage, as cost depends on the same variables that influence any automobile premium. Rather than citing a fixed figure, which varies considerably by state and insurer, it is more instructive to examine the factors that raise or lower the premium.

Factors affecting the premium

- Driving record: Violations, prior accidents, or a DUI/DWI conviction increase the premium significantly.

- Location: The state and ZIP code of the insured affect pricing.

- Coverage limits: Higher liability limits cost more but provide greater protection.

- SR-22 requirement: A required SR-22 filing adds fees and typically raises the premium.

- Insurer: Nonstandard carriers price these policies differently, so quotes should be compared.

Illustrative average costs

Although prices vary widely, published industry data offer a useful benchmark. One 2026 analysis reported an average broad form premium of approximately $768 per year, or about $64 per month, with rates differing considerably among carriers; the same analysis identified USAA, Progressive, and Nationwide among the most affordable providers. The figures below are illustrative averages for minimum-level coverage and should be treated as a starting point for comparison rather than a quotation.

| Insurer | Reported average monthly cost (minimum coverage) |

|---|---|

| USAA | $50 |

| Progressive | $59 |

| Nationwide | $63 |

| Travelers | $67 |

| Allstate | $72 |

| Liberty Mutual | $74 |

Broad form car insurance vs standard, non-owner, and full coverage

To situate broad form coverage among its alternatives, the following comparison contrasts it with non-owner car insurance, standard minimum (liability-only) coverage, and full coverage. The table clarifies which protections each option provides and the type of driver each is designed to serve.

| Feature | Broad form | Non-owner | Liability-only (minimum) | Full coverage |

|---|---|---|---|---|

| Meets state minimum liability | Yes | Yes | Yes | Yes |

| Higher liability limits available | No | Yes | Yes | Yes |

| Collision / comprehensive | No | No | No | Yes |

| Who is covered | Named insured only | Named insured (and co-insured) | Named, listed, and occasional drivers | Named, listed, and occasional drivers |

| Vehicles covered | Those are the named driver operates | Borrowed or rented vehicles | The insured’s own and third parties | The insured’s own and third parties |

| Reported typical monthly cost | $64 | $83 | $100 | $216 |

| Best suited for | Sole drivers of low-value cars | Drivers who do not own a vehicle | Owners of older, paid-off cars | Owners of newer, financed, or leased cars |

Who should consider broad form car insurance?

The product may appeal to drivers seeking cheap car insurance with basic liability protection, but it is suitable only for a narrow group who drive alone and understand the associated financial risks.

The most suitable candidate is generally a single driver who owns an older, low-value vehicle and does not permit others to operate it. For such an individual, broad form coverage may merit comparison against a standard liability-only policy.

Broad form coverage may be appropriate when the driver:

- Is the sole operator of the vehicle.

- Does not share the vehicle with family members, friends, or roommates.

- Owns an older vehicle of limited market value.

- Can afford to repair or replace the vehicle out of pocket.

- Requires only basic liability protection.

- Owns more than one vehicle but is the sole driver, since a single broad form policy can cover multiple owned cars without a higher premium.

- Resides in a state where broad form coverage is permitted.

Broad form coverage may be inappropriate when the driver:

- Shares the vehicle with a spouse, partner, or teenage driver.

- Permits friends or roommates to borrow the vehicle.

- Finance or lease the vehicle.

- Requires full coverage protection for the vehicle itself.

- Cannot absorb significant repair or replacement costs.

- Must ensure multiple drivers or multiple vehicles.

Pros and cons of broad form car insurance

The value of broad form coverage depends on whether its limitations align with the policyholder’s circumstances, much as with other low-cost financial products.

Advantages

- Generally less expensive than standard automobile insurance.

- Simple structure suited to a single driver.

- May satisfy basic liability requirements.

- May be appropriate for older, low-value vehicles.

- Avoid paying for optional coverages that are not needed.

Disadvantages

- Covers only one named driver.

- Excludes other operators of the insured vehicle.

- Does not cover damage to the insured’s own vehicle.

- Typically omits collision and comprehensive coverage.

- May not satisfy lender or lease requirements.

- Is unavailable in most states.

- May provide inadequate protection after a serious accident.

The most common error is to regard broad form coverage as merely an inexpensive version of a standard policy. It is, in fact, a distinct product with a different risk profile.

How to get broad form car insurance quotes

A driver seeking car insurance for one driver should first determine whether broad form policies are available in the relevant state, since availability is limited and regulated differently across jurisdictions.

Step 1: Confirm availability

Confirm with insurers or licensed agents whether broad form coverage is offered in the state, whether it is a named-driver policy, whether it satisfies state minimum requirements, and whether vehicle restrictions apply.

Step 2: Compare coverage line by line

Before choosing based on price alone, make sure you know how to get auto insurance quotes using the same liability limits, named-driver restrictions, deductibles, and exclusions. Comparison should extend beyond the monthly payment to liability limits, covered drivers, covered vehicles, exclusions, optional coverages, SR-22 availability, cancellation provisions, and the claims process.

Step 3: Compare against standard auto insurance

Obtain at least one quote for a standard liability-only policy, together with the cost of adding collision and comprehensive coverage. In some instances, the price difference is modest, and the broader policy represents better value.

Step 4: Select based on risk

If the applicant is the sole driver and can absorb the cost of repairing or replacing the vehicle, broad form coverage may be reasonable. If any other person is likely to operate the vehicle, the decision warrants careful reconsideration.

Alternatives to broad form car insurance

Drivers who cannot purchase broad form coverage, or who require broader protection, have several alternatives. In addition to the standard minimum-liability and non-owner car insurance options discussed above, certain states operate low-income automobile insurance programs for qualifying residents. Eligibility criteria, including income and driving history, differ by program.

- California: California Low Cost Automobile Insurance Program (CLCA)

- New Jersey: Special Automobile Insurance Policy (SAIP)

- Hawaii: Assistance to the Aged, Blind and Disabled program (AABD)

- Maryland: Maryland Auto Insurance

RELATED AUTO INSURANCE GUIDES

Auto Insurance

Is auto insurance tax deductible? 2026 guide for drivers

Auto Insurance

Does auto insurance cover hail damage? What to do next

Auto Insurance

Does auto insurance cover rental cars? 2026 guide

Auto Insurance

When does a car become a classic for insurance 2026?