If you were told you need an SR-22, it usually means your state wants proof that you carry the required auto liability coverage before you can legally drive or reinstate your license. Many drivers first hear about SR-22 after a DUI/DWI, driving without insurance, a suspended license, or another serious violation.

The confusing part is that people often call it “SR-22 insurance,” even though it is not a separate insurance policy. It is a state-required filing attached to an auto policy, and the rules can vary depending on where you live.

Auto Insure News breaks down what that filing actually means, who usually needs it, how the process works, how much it may add to your insurance cost, how long you may need to keep it, and why keeping your coverage active is so important.

What is SR-22?

SR-22 is a certificate, not an insurance policy. The “SR” stands for Safety Responsibility. Formally known as a Certificate of Financial Responsibility, an SR-22 is a document that your insurance company files with your state’s Department of Motor Vehicles on your behalf. Its sole purpose is to prove to the state that you are carrying at least the minimum required auto liability coverage mandated by law. One of the most important car insurance facts to understand is that “SR-22 insurance” is not actually a separate insurance policy. The SR-22 itself is a state-required filing attached to an auto liability policy, used to prove that you carry at least the minimum required coverage.

How SR-22 works

An SR-22 works as a monitoring mechanism between your insurance company and the state. Once an SR-22 is required, your insurer files the certificate with the DMV to verify that you carry at least the minimum liability coverage required by law. If your policy remains active, the SR-22 stays on file and helps maintain your driving privileges. However, if the policy is canceled, non-renewed, or lapses, the insurer must notify the state, which may suspend your license or require additional proof of financial responsibility before you can legally drive again.

Who needs an SR-22?

Drivers usually need an SR-22 after a state DMV, court, or motor vehicle agency determines they must prove future financial responsibility. Common triggers include DUI/DWI, driving without insurance, a suspended or revoked license, reckless driving, an uninsured accident, or a court judgment after a crash.

When is an SR-22 required?

Here are the most common reasons a driver is required to file an SR-22:

- DUI or DWI conviction – One of the most common reasons for an SR-22 or similar financial responsibility filing.

- Driving without insurance – If you were caught operating a vehicle without any liability coverage, the state will likely require proof of future financial responsibility.

- License suspension or revocation – An SR-22 is often a mandatory requirement for getting your suspended license reinstated, regardless of why it was suspended.

- Reckless driving conviction – Classified as a serious moving violation, reckless driving frequently triggers an SR-22 requirement in most states.

- At-fault accident while uninsured – Being involved in an accident and having no insurance is a fast path to an SR-22 mandate.

- Excessive traffic violations – Accumulating too many points on your driving record within a short period can cause the DMV to classify you as a high-risk driver and require an SR-22.

- Failure to pay court-ordered judgments – In some states, failing to pay damages from an accident judgment can also lead to an SR-22 requirement.

How much does SR-22 cost?

The SR-22 filing fee

The SR-22 form itself is usually inexpensive. Many insurers charge about $15 to $35 to file the form, though the fee varies by state and insurer. Some companies charge it upfront, include it in your premium, or charge it each policy term while the SR-22 requirement remains active. Either way, the filing fee is usually minor compared with the premium increase caused by the underlying violation.

Does an SR-22 Increase Insurance Rates?

The true cost of an SR-22 is the significant increase to your auto insurance rates that comes with being reclassified as a high-risk driver. A violation triggers your SR-22 filing requirement – and it is that violation, not the form itself, that causes your premiums to spike.

Here is what the data shows for 2025:

SR-22-related insurance increases vary widely because the surcharge is usually driven by the violation that triggered the filing, not by the SR-22 form itself. For example, The Zebra’s SR-22 insurance data shows average annual premium increases of about $1,092 after a DUI, $1,054 after reckless driving, $940 after driving with a suspended license, and $687 after an at-fault accident with more than $2,000 in damage. Actual increases depend on your state, insurer, driving history, coverage level, and ZIP code.

According to Insurance.com’s 2026 analysis, drivers with an SR-22 pay about $1,511 more per year on average, although the actual increase can be much higher or lower depending on the violation, state, insurer, and coverage level. Over a typical three-year filing period after a DUI, total extra premium costs can reach $4,000 to $8,000 – far more meaningful than the $25 filing fee.

How to reduce your SR-22 insurance costs:

- Shop and compare quotes from at least three carriers that accept SR-22 filings. Rate differences between insurers for high-risk drivers can be substantial.

- Ask about telematics or usage-based insurance programs – some carriers will lower your rate based on demonstrated safe driving behavior over 6–12 months.

- Keep your driving record clean throughout the SR-22 period. Additional violations can increase your premiums, trigger new penalties, or extend your financial responsibility requirement depending on state law.

- Review your coverage levels – you are required to carry state minimums, but you are not required to carry more than that if cost is a priority.

How long do you need SR-22?

The SR-22 requirements by state vary more than most people realize. While the standard filing period is three years, the actual duration depends on both your state’s law and the severity of the underlying offense. Knowing your specific timeline helps you plan and avoid costly mistakes.

One important rule applies in every SR-22 case: you must maintain continuous coverage for the full required period. If your policy lapses, is canceled, or is non-renewed, your insurer must notify the state. The result can include license suspension, reinstatement fees, and a new filing requirement. In some states or cases, a lapse may also extend or restart the required filing period, so drivers should confirm the exact consequence with their state DMV. That makes maintaining uninterrupted coverage the single most important task during your SR-22 period.

SR-22 Duration by State (Selected Examples):

| Required Duration | States |

|---|---|

| 1 year | North Dakota |

| 2 years | Texas, Iowa |

| 3 years (standard) | 26 states – the most common requirement |

| 3–5 years | Alabama, Arkansas, Indiana, Ohio, Tennessee |

| Up to 5 years | Nebraska (DUI), Tennessee (DUI) |

| Up to 20 years | Alaska (multiple repeat offenses) |

How to get an SR-22?

Obtaining an SR-22 is usually a straightforward process. While the filing itself is handled by your insurer, drivers still need to meet their state’s insurance requirements and maintain continuous coverage throughout the filing period.

Step 1 – Receive official notification. You will get a written notice from a court or your state DMV specifying that an SR-22 is required. This notice will include a deadline and may list the minimum liability limits your policy must meet.

Step 2 – Contact your insurance company. Call your insurer and tell them you need an SR-22 filing attached to your policy.

Here is a critical point most guides miss: not every insurance company handles SR-22 filings. Some insurers – particularly those that specialize in preferred or low-risk drivers – do not offer this service. If your current insurer does not file SR-22s, you will need to switch to one that does. Major carriers, including Progressive, State Farm, and GEICO, all handle SR-22 filings.

Important: If you need to switch insurers, do not cancel your old policy until the new policy is active and the SR-22 has been filed with your state. A lapse, cancellation, or non-renewal can cause your insurer to notify the DMV, which may lead to another license suspension or reinstatement problem.

Step 3 – Confirm your coverage meets state minimums. Your existing policy must meet or exceed your state’s minimum liability limits, so review the basic coverage parts of an auto policy before assuming your current limits are enough. If it does not, you will need to increase your coverage before the SR-22 can be filed.

Step 4 – Pay the SR-22 filing fee. The fee for the SR-22 form itself is modest – typically $15 to $35, paid to your insurance company. Some insurers roll this into your premium; others charge it separately at the time of filing.

Step 5 – Your insurer files the SR-22 electronically. Once everything is in order, your insurance company submits the SR-22 form directly to your state’s DMV. Electronic filing is the norm today, and most insurers can complete this within 24 to 72 hours. Some provide same-day filing. You should receive a copy of the certificate for your own records.

Step 6 – Maintain continuous coverage. Keep your SR-22 policy active for the full required filing period. If your policy is canceled, non-renewed, or lapses, your insurer may notify the state, and your license may be suspended again. Set up automatic payments and confirm the new SR-22 filing before switching insurers.

Step 7 – Request removal when your filing period ends. Once you have completed the required filing period (usually three years), the SR-22 is not automatically removed from your record. You must contact your insurer and ask them to stop filing the SR-22 with the DMV-more on this in the removal section below.

SR-22 vs. FR-44: What’s the Difference?

Understanding these state variations for high-risk driver insurance compliance can save you from accidentally assuming you have satisfied a requirement when you have not.

States that do not use SR-22:

Not every state uses the SR-22 system. Several insurance sources list Delaware, Kentucky, Minnesota, New Mexico, New York, North Carolina, Oklahoma, and Pennsylvania as states that do not require SR-22 filings for residents after a violation. However, SR-22 rules can change and may depend on the driver’s original state order. If you were required to file an SR-22 in another state and then move, you generally still need to satisfy the original state’s requirement until it ends.

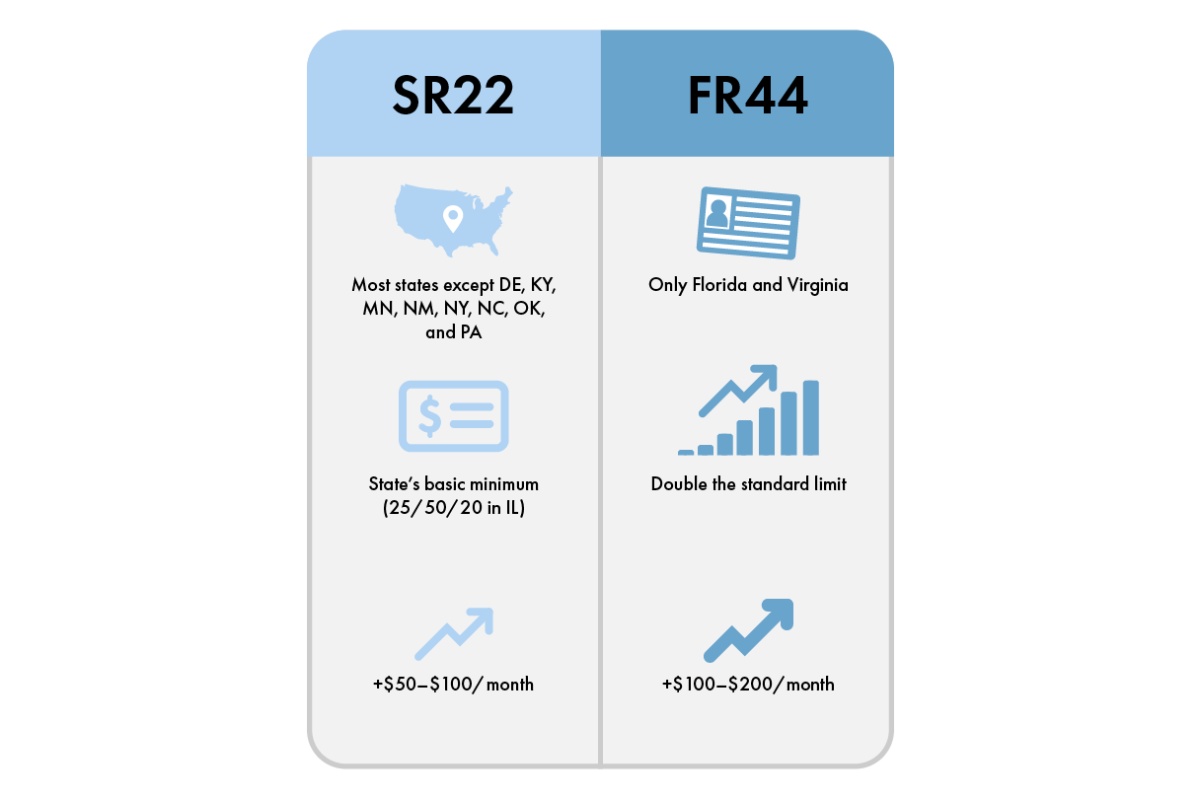

FR-44: The Stricter Version Used in Florida and Virginia

Florida and Virginia use FR-44 filings for certain serious alcohol- or drug-related driving offenses, including DUI/DWI. Like an SR-22, an FR-44 is a certificate of financial responsibility filed by your insurer, but it requires higher liability limits than a standard SR-22 filing.

| Feature | SR-22 | FR-44 |

|---|---|---|

| States Used | Most states require financial responsibility filings | Florida and Virginia |

| Who Needs It | Drivers with certain serious violations, depending on state law | Drivers with certain serious alcohol- or drug-related offenses, depending on state law |

| Coverage Required | Usually state minimum liability coverage | Higher liability limits than a standard SR-22 |

| Florida Limits | Standard Florida SR-22 limits may apply for non-DUI cases | 100/300/50 for qualifying DUI cases |

| Virginia Limits | Virginia minimum liability limits | Double Virginia’s minimum liability limits; 100/200/50 for policies effective Jan. 1, 2025, or later |

| Premium Impact | The filing fee is small, but the violation can raise premiums | Usually higher because the driver may need higher liability limits |

If you are in Florida or Virginia and received a DUI or similar alcohol- or drug-related conviction, you may be required to file an FR-44 instead of an SR-22. Check your DMV notice or court order to confirm the exact filing required.

What is a non-owner SR-22?

A non-owner SR-22 is one of the most misunderstood yet practical options available to drivers who need to satisfy an SR-22 requirement but do not currently own a vehicle. It is more common than you might think – plenty of drivers lose their license, surrender their car, and still need to reinstate their driving privileges.

If you find yourself in this situation, a non-owner auto insurance policy with an SR-22 filing attached is exactly what you need. This type of policy provides liability-only coverage for vehicles you borrow, rent, or occasionally drive – without insuring a specific car you own. It satisfies the state’s SR-22 requirement fully, and it keeps your costs lower than a standard full-coverage policy since there is no vehicle asset to insure.

Here is what you need to know about non-owner SR-22 policies:

- They provide liability-only coverage – injuries and property damage to others, not damage to the vehicle you are driving

- They are available from some insurers, including major carriers that offer non-owner policies and SR-22 filings. Pricing varies widely by state, violation, insurer, age, and driving history, so compare quotes from multiple companies instead of relying on a single national estimate.

- A non-owner SR-22 can satisfy the filing requirement if you do not own a vehicle, but the filing period and start date are controlled by your state or court order.

- If you later purchase a vehicle, you will need to transition to a standard auto insurance policy with the SR-22 filing transferred over

What happens if your SR-22 lapses?

The SR-22 and license suspension risk is never higher than when your policy lapses during your filing period – and this is exactly where many drivers make a costly mistake. Missing a payment, switching insurers carelessly, or simply letting your policy expire without renewing can undo months or years of progress.

This is not a minor administrative issue. If your auto insurance policy lapses or is cancelled while you have an active SR-22 requirement, the following consequences may happen, depending on your state’s rules:

- Your insurer notifies the state if your SR-22 policy is canceled, non-renewed, or lapses. The reporting timeline depends on state rules and insurer procedures, but the consequence can be serious: the DMV may suspend your license or require you to file new proof of financial responsibility before you can legally drive again.

- Your driver’s license may be suspended. Once the state receives notice that your SR-22 is no longer valid, it may suspend your license until you provide valid proof of financial responsibility again.

- Your SR-22 requirement may be extended, restarted, or remain unresolved until you file valid proof again, depending on your state’s rules. Do not assume the time you have already completed will automatically count after a lapse. Contact your DMV before restarting coverage so you know exactly how your state treats the interruption.

- You face additional reinstatement costs. Getting your license reinstated requires a new SR-22 filing plus reinstatement fees averaging $100 to $300, depending on your state – on top of the increased insurance costs you will already be paying.

How to prevent an SR-22 lapse:

- Enroll in automatic payments through your insurer

- Set a calendar reminder 60 days before your policy renewal date

- If you switch insurers, ensure the new policy and SR-22 filing are active before cancelling your old policy – never let there be a single day of gap in coverage

- Keep your insurer’s contact information accessible and respond immediately to any renewal notices

How to remove SR-22 from your insurance

Once you have completed your required filing period, you naturally want to know how to remove SR-22 from your record and get back to standard insurance rates. The good news: removal is straightforward. The reality check: some effects linger longer than the filing itself.

When you are approaching the end of your SR-22 filing period, understanding the removal process helps you time it correctly and avoid paying for the filing longer than required.

Here is what the removal process looks like:

- SR-22 is not removed automatically. When your filing period ends, nothing happens on its own. The certificate stays attached to your policy until you take action.

- Contact your insurer directly and request that they stop the SR-22 filing with your state’s DMV. This is a simple request that your insurer should be able to process quickly.

- Check your state’s process. Some states issue a formal clearance letter or release form confirming you have satisfied the requirement. Others update your license status in their system automatically upon receiving the insurer’s notification to stop filing. Your state DMV can confirm which process applies to you.

- Do not rely on your insurer to remove the SR-22 automatically or remind you before the requirement ends. Contact your state DMV or your insurer near the end of the filing period to confirm the exact end date, then ask your insurer to remove the SR-22 filing once you are cleared.

Important: your rate may not drop immediately after the SR-22 filing is removed. The SR-22 is only the administrative filing; the underlying violation, such as a DUI or reckless driving conviction, may remain on your driving record longer than the SR-22 period and can continue affecting your insurance rate at renewal. How long it affects pricing depends on your state, insurer, and violation.

Once the violation ages off your record completely, you should shop your insurance aggressively – that is when you will see the most significant rate reductions.

RELATED AUTO INSURANCE GUIDES

Auto Insurance

Is auto insurance tax deductible? 2026 guide for drivers

Auto Insurance

Does auto insurance cover hail damage? What to do next

Auto Insurance

Does auto insurance cover rental cars? 2026 guide

Auto Insurance

When does a car become a classic for insurance 2026?